AI for Mortgage Brokers: Close 3x More Deals With Automated Lead Nurturing, Pre-Qualification & Onboarding

The Revenue Drain Hidden Inside Your Pipeline

You receive a lead on a Saturday afternoon. The buyer enquired through three brokers at once — yours, a competitor down the road, and a direct bank. You see it Monday morning and send a friendly email. Your competitor had an AI bot respond within 60 seconds Saturday afternoon, collected the buyer's income details, and booked a consultation call for Sunday evening. By Monday, they have a pre-qualified client. You have an unread email.

This scenario plays out thousands of times every week across the mortgage industry. Speed-to-lead is not just a sales tactic — it is the single biggest driver of conversion in financial services. Research by InsideSales.com shows that responding to a lead within 5 minutes makes you 21 times more likely to convert than responding after 30 minutes. The average manual broker response time is 4.2 hours.

But the problem does not stop at lead response. Mortgage brokers also lose deals through slow pre-qualification, stalled document collection, and — the silent killer — failure to re-engage past clients at renewal. A broker with 200 settled clients who does not have a renewal re-engagement system in place is leaving $180,000–$400,000 in trail commission and new deal fees on the table annually.

AI automation closes every one of these gaps. This guide covers the four workflows that matter most, the tools available in 2026, the implementation sequence, and the exact ROI numbers brokers are reporting.

Key Takeaway

Mortgage brokers who respond to leads within 5 minutes are 21x more likely to convert them. AI automation makes sub-90-second response time the default — at any hour, without hiring additional staff.

Explore all industry-specific AI automation solutions we offer at Jogi AI.

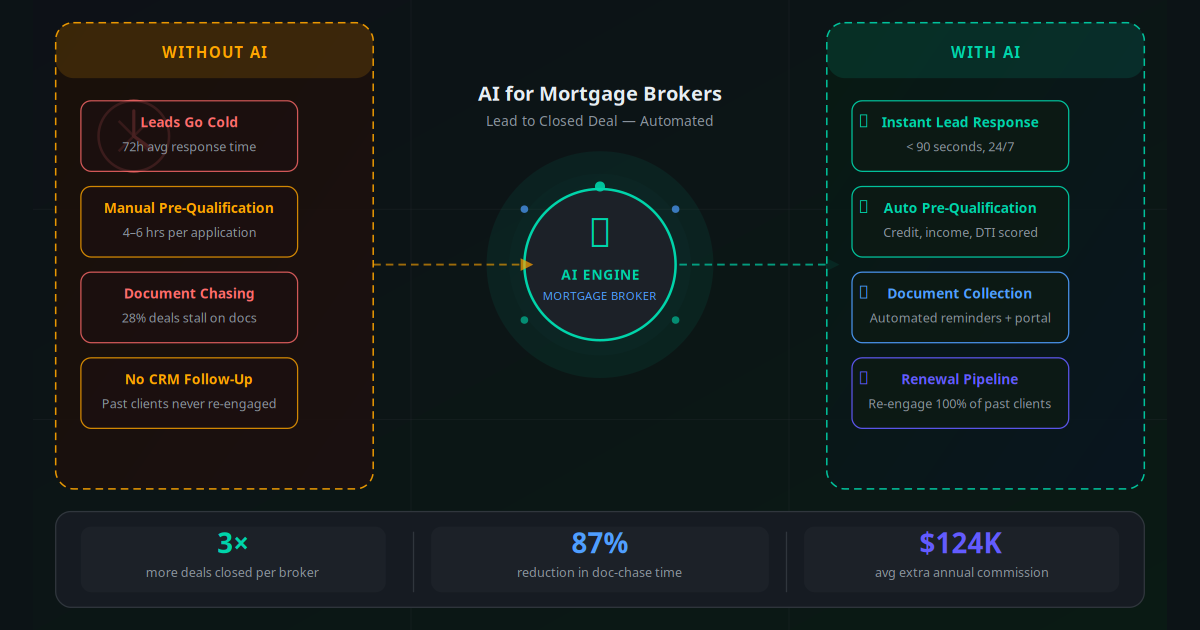

What AI Actually Does for a Mortgage Broker

There is an important distinction between AI that answers questions and AI that runs workflows. What transforms a mortgage brokerage is the second type: AI that executes sequences of actions triggered by specific events in your pipeline.

Here is a plain-English breakdown of what AI does across the mortgage workflow:

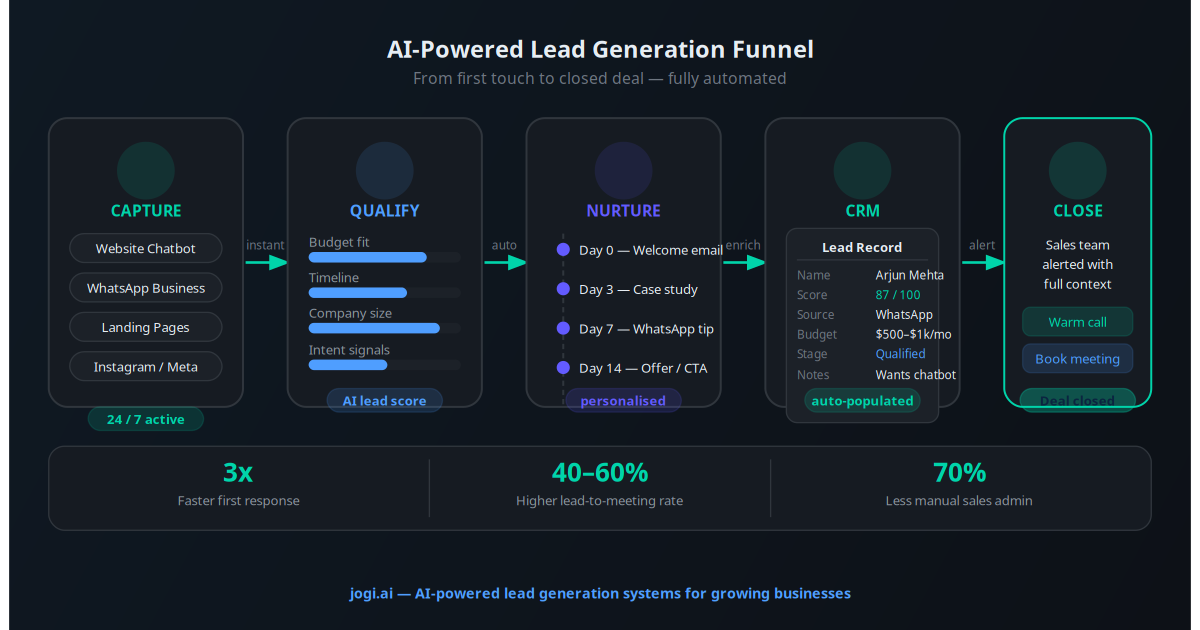

- Lead capture and instant response: A chatbot or WhatsApp AI engages every inbound enquiry within 60–90 seconds, collects structured qualifying data, and either books a broker call or flags the lead as not yet ready.

- Pre-qualification scoring: The AI compares the collected data (income, deposit, employment type, credit signals, existing debt) against your lender panel criteria and assigns a qualification score — before a broker spends a minute on the file.

- Application document collection: Automated multi-channel reminders chase outstanding documents (payslips, bank statements, ID) via SMS, email, and WhatsApp — stopping only when every document is received.

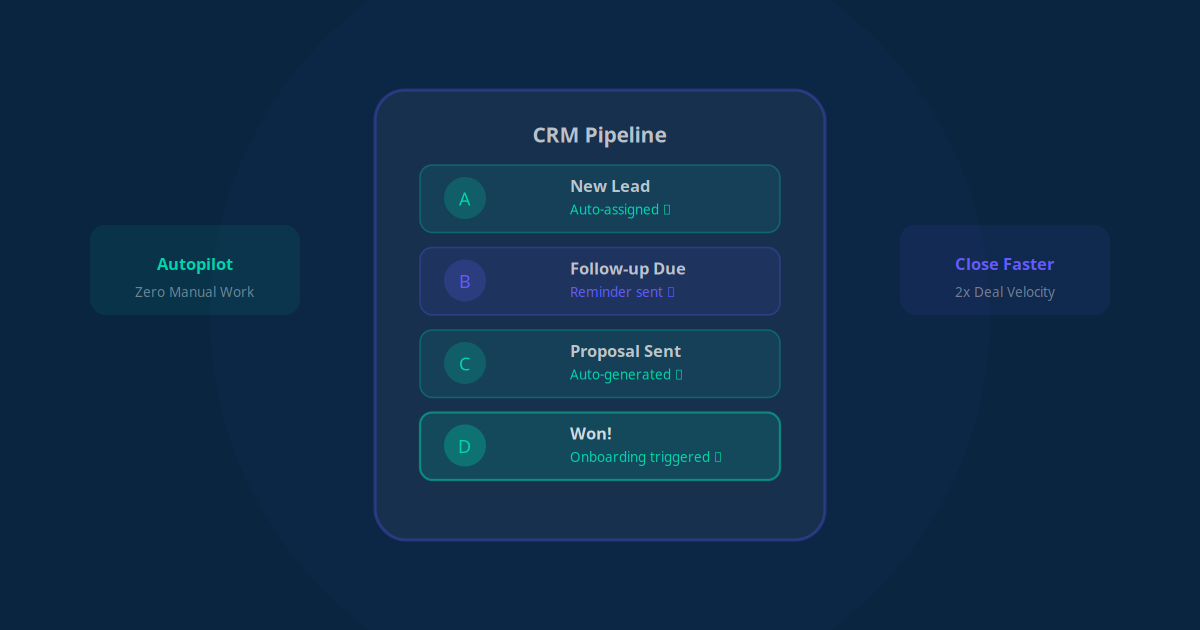

- CRM pipeline management: Every touchpoint, document, and stage change is logged automatically. Your CRM shows you exactly where each deal is without anyone updating it manually.

- Renewal and refinance re-engagement: The AI monitors every client's fixed-rate expiry or standard variable rate rollover date and triggers a personalised outreach sequence 90, 60, and 30 days out.

- Post-settlement follow-up: Automated check-ins at 3, 6, and 12 months post-settlement maintain the relationship, surface referral opportunities, and keep your brand top-of-mind.

None of this replaces the broker's regulated role in advice, product comparison, and client suitability assessment. What it removes is the 60–70% of broker time currently spent on admin, chasing, and manual follow-up — time that could go toward high-value client work and new business development.

Workflow 1 — Instant Lead Response and Qualification

Every referral website, comparison portal, social ad, or Google search that sends a lead to your brokerage triggers the same first question: how fast can you respond, and how much useful information can you collect before that lead goes cold?

An AI lead response system handles this automatically. When a prospect submits a contact form, sends a WhatsApp message, or calls outside business hours, the AI engages them immediately — introducing your brokerage, explaining the process, and asking the four to six questions that determine whether they are ready to proceed.

What the AI collects in the first conversation

- Purchase or refinance intent, and property type

- Estimated property value and deposit or equity amount

- Employment status (PAYG, self-employed, contractor)

- Gross annual income and existing monthly debt commitments

- Current mortgage if refinancing — lender, rate, and expiry

- Timeline (ready now, 3 months, 12 months)

With that data, the AI scores the lead, tags it in your CRM, and either books a consultation in your calendar or places the prospect into a nurture sequence if they are not yet ready to proceed. The broker wakes up to a qualified pipeline — not a list of cold contact form submissions.

Brokers who automated their lead response reported a 34% increase in consultation bookings from the same lead volume — without changing their marketing spend.

This workflow connects directly with CRM automation and WhatsApp Business automation — both of which are central to how AI-powered mortgage brokerages manage their pipeline at scale.

Workflow 2 — Automated Pre-Qualification Scoring

Pre-qualification is where most brokers lose hours. A file arrives, you request details, the client sends partial information, you follow up, they forget, you chase again. Three days later you have enough to run affordability numbers manually — and by then the client's enthusiasm has cooled.

AI pre-qualification changes this from a multi-day back-and-forth into a 15-minute structured intake. The AI sends the client a branded digital questionnaire (or conducts the intake conversationally via WhatsApp), collects all necessary data, and runs it through your affordability model automatically.

What the scoring engine checks

- Loan-to-value (LTV) ratio: Deposit or equity against purchase price or estimated value

- Debt-to-income (DTI) ratio: Total existing debt commitments as a percentage of gross income

- Employment stability: Time with current employer, contract type, any gaps in employment history

- Lender product match: Which lenders on your panel accept the applicant profile (e.g. self-employed with 1-year accounts, high LTV first-time buyers, interest-only applicants)

- Credit signal indicators: Defaults, CCJs, late payments — disclosed by the client and cross-referenced against lender criteria

The output is a traffic-light score: green (proceed to full application), amber (proceed with specified conditions), or red (not ready — place in nurture). Your broker reviews the AI's output in 3 minutes rather than spending 45 minutes collecting and calculating it themselves.

Key Takeaway

AI pre-qualification reduces the average time a broker spends per application from 4–6 hours of initial admin to under 30 minutes of review — freeing capacity for 3x as many active files.

Workflow 3 — Document Collection Without the Chasing

Document collection is the mortgage industry's biggest bottleneck. The average time from initial application to complete file submission is 11 days — and 28% of that delay comes from clients who fail to submit required documents on the first request.

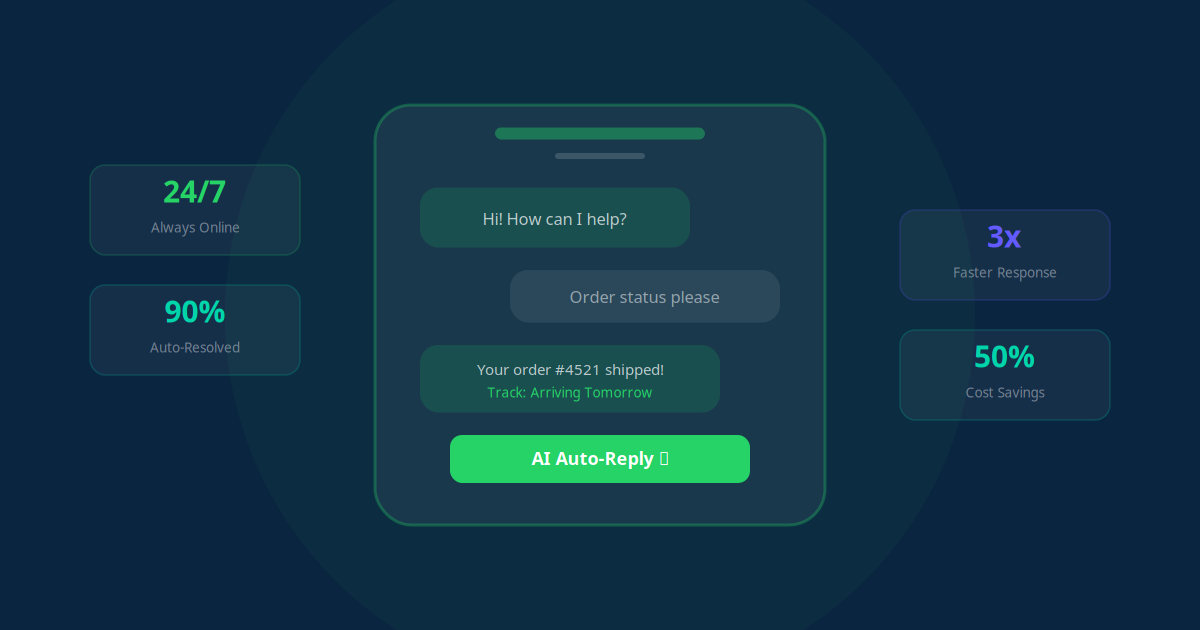

The problem is not that clients are unwilling. It is that collecting documents feels complex and urgent to the broker but low-priority and confusing to the client. A reminder email from a broker sits in the same inbox as 200 other emails. A WhatsApp message from your brokerage's AI assistant — with a one-tap secure upload link and a clear list of exactly what is outstanding — gets actioned the same day.

Here is how an automated document collection system works in a mortgage brokerage:

Application initiated: AI generates a personalised document checklist based on the applicant's profile (PAYG vs self-employed, purchase vs remortgage, LTV tier). The checklist is sent immediately via email and WhatsApp with a secure portal link.

Day 1 reminder: If the portal has not been accessed within 24 hours, a friendly reminder WhatsApp message is sent: "Hi [Name], your file for [address] is ready — just tap here to upload your documents. It only takes 5 minutes."

Day 3 follow-up: AI sends a progress update showing which documents have been received and which are still outstanding — reducing client anxiety and making the remaining task feel smaller.

Day 5 escalation: An SMS is sent for any documents still outstanding, with a specific call to action. If no response, the broker is automatically notified to make a personal call.

File complete alert: The moment all required documents are received, the broker receives an instant notification with a link to the complete file — ready for lender submission without any admin work.

Lender submission tracking: Post-submission, AI tracks lender response times, flags any requests for additional information, and triggers the appropriate client communication automatically.

Conditional approval workflow: When a conditional approval arrives, AI notifies the client, explains the conditions in plain English, and initiates collection of any additional documentation required — without broker involvement.

Brokers using this workflow report cutting average document collection time from 11 days to under 3 days — an 87% reduction in the time this bottleneck adds to the pipeline. The connection with AI workflow automation principles is clear: the AI does not eliminate the steps, it eliminates the waiting.

Workflow 4 — Renewal and Refinance Re-Engagement

Here is a number that should concern every mortgage broker: only 22% of clients with a fixed-rate expiry proactively contact their original broker. The other 78% either go directly to their existing lender's renewal offer (often uncompetitive), find a new broker, or let their loan roll to a standard variable rate — paying thousands more per year.

This is not a loyalty problem. It is a timing and communication problem. Most clients do not know their rate is expiring until they receive a letter from the lender — by which point the lender has already pre-empted the retention decision. An AI renewal system ensures you get there first, every single time.

The system works by pulling renewal dates from your CRM and triggering a multi-touch sequence that begins 90 days before expiry:

- Day 90: Personalised email — "Your fixed rate with [Lender] expires on [Date]. Here is what that means for your repayments and what we recommend you consider."

- Day 60: WhatsApp message with a booking link — "It is a great time to review your options. I have 15 minutes available this week to walk you through the current market rates."

- Day 30: SMS with urgency — "Your rate expires in 30 days. Locking in a new deal now could save you $[calculated amount] per month."

- Day 14: Personal broker notification if no response — prompting a direct call before the rate rolls over.

Brokers who implement this system consistently capture 65–70% of their existing book for renewal discussions, compared to 22% without automation. For a broker with 300 settled loans averaging $500,000, that translates to $240,000 in annual trail commission that would otherwise be lost.

The AI-powered lead generation principles that work for new business apply equally to existing client retention — the best pipeline you have is the one you already closed.

Real-World Use Cases by Broker Type

Residential Purchase Broker — First-Home Buyer Specialist

A first-home buyer broker receives 60–80 enquiries per month from comparison sites and Google Ads. Without automation, each enquiry requires a manual callback to qualify. With an AI lead response bot, every enquiry is engaged within 90 seconds, first-home buyer eligibility is assessed automatically (government scheme eligibility, stamp duty concessions, genuine savings), and only genuinely ready buyers are booked for broker calls. The broker reduced unqualified consultations by 61% and increased the settlement rate on consultations from 34% to 58%.

Commercial Mortgage Broker — SME Property Finance

Commercial mortgage enquiries require detailed upfront information — business financials, property use, LVR, serviceability. An AI pre-qualification intake collects full financials, existing debt structure, and property details before the broker's first contact. The broker enters every call with a complete picture of the deal. Time spent per initial consultation dropped from 2 hours to 45 minutes, and the broker increased active files under management from 12 to 31 without additional staff.

Refinance Specialist — Rate and Cashback Campaigns

A refinance-focused brokerage runs regular rate-drop campaigns via email and SMS to their past client database. When a recipient clicks through, an AI chatbot immediately qualifies them (current rate, remaining term, estimated equity, credit signals) and books a consultation if they are a viable refinance candidate. Campaign conversion from click to booked consultation increased from 11% to 29% after switching from a static contact form to an AI qualification chat.

Multi-Broker Firm — Team Pipeline Management

A firm with 8 brokers was losing deals because pipeline visibility was poor — leads fell through cracks between brokers, follow-ups were inconsistent, and no one knew which broker had last contacted which client. AI CRM automation now logs every touchpoint automatically, assigns leads based on broker capacity and specialisation, and escalates any lead that has not been contacted within 4 hours. Deal leakage dropped from 23% to 4% of inbound leads within 60 days of implementation.

Independent Broker — Full Automation Stack

A sole-operator broker with no administrative support automated lead response, pre-qualification, document collection, and renewal re-engagement. The time saved per week — previously consumed by email, phone tag, and manual CRM updates — was approximately 22 hours. That time was reinvested into broker education, referral partner relationships, and a LinkedIn content strategy that added 4 new referral sources within 90 days.

How to Implement AI in Your Brokerage: 7-Step Plan

The most common mistake brokers make is trying to automate everything at once. Start with lead response — it has the fastest visible ROI — then layer additional workflows over 60–90 days.

Audit your current lead sources: List every channel that sends you enquiries (comparison sites, Google Ads, referrals, social media). Identify where the gaps are — which sources have the longest response times and lowest conversion rates. These become your first automation targets.

Set up your CRM if you have not already: AI automation is only as useful as the CRM it feeds. If you are managing leads in a spreadsheet, migrate to a CRM (HubSpot Free, Pipedrive, or a mortgage-specific CRM) before adding automation layers. This is non-negotiable.

Deploy the lead response chatbot (Week 1–2): Install a chatbot on your website and connect it to your WhatsApp Business number. Program it with your pre-qualification questions and your calendar booking link. Connect it to your CRM so every new lead is automatically created with the collected data. Test it with 10 mock enquiries before going live.

Build the pre-qualification intake form (Week 2–3): Create a branded digital intake form covering all the information you need before a consultation. Connect form completion to an automated email sequence that delivers the broker's pre-consultation checklist to the client. Map the form output to your CRM fields so pre-qual scores populate automatically.

Implement document collection automation (Week 3–4): Choose a document portal (Dext, FileInvite, or a custom-built solution) and set up the automated reminder sequences. Configure the reminder cadence, the channels (email, SMS, WhatsApp), and the broker escalation trigger. Connect document receipt to CRM stage updates.

Build the renewal re-engagement sequence (Week 5–6): Pull all fixed-rate expiry dates from your existing client records into your CRM. Create the 90/60/30/14-day email and WhatsApp sequences with personalised rate comparison data. Set the triggers and test with a small cohort of upcoming renewals before rolling out to your full book.

Monitor, measure, and refine (Ongoing): Track four metrics weekly: lead response time, consultation booking rate, document collection completion time, and renewal re-engagement rate. Set benchmarks based on your first 30 days of data and review monthly. The AI improves as you refine the scripts and intake questions based on real interaction data.

AI Tools and Platforms for Mortgage Brokers in 2026

| Tool / Platform | Primary Use Case | Approx. Monthly Cost | Mortgage Broker Fit |

|---|---|---|---|

| HubSpot CRM (Free–Growth) | Pipeline management, email sequences, deal tracking | $0–$800 | Strong — native automation, great free tier |

| Pipedrive + AI Add-on | Visual pipeline, lead scoring, email automation | $25–$100 per user | Strong — built for sales teams, broker-friendly UI |

| Make.com (Integromat) | Workflow automation between apps | $9–$99 | Strong — connects CRM, email, WhatsApp, document portals |

| Tidio / Intercom | Website chatbot and lead qualification | $29–$149 | Good — quick to deploy, connects to most CRMs |

| FileInvite | Document collection and reminders | $29–$119 | Excellent — purpose-built for professional services doc collection |

| ActiveCampaign | Email and SMS automation sequences | $29–$149 | Strong — renewal sequences, post-settlement nurture |

| WhatsApp Business API | Automated messaging across all pipeline stages | Per message + platform | Essential — highest response rates of any channel |

| Jogi AI Full Stack | End-to-end automation: CRM, chatbot, WhatsApp, sequences | From $179 | Excellent — designed for SMB service businesses end-to-end |

For brokers evaluating automation platforms more broadly, the Make vs Zapier vs n8n comparison is worth reading — it covers the integration layer that connects your CRM, document portal, and communication channels into a coherent automated pipeline. For chatbot technology specifically, the guide to RAG AI assistants for smarter chatbots explains how to build a pre-qualification bot that pulls from your actual lender criteria and product knowledge base rather than giving generic answers.

The ROI Picture: What Brokers Are Actually Seeing

"I went from settling 4 deals a month to 11 — without hiring anyone. The automation handles everything I used to do manually between 5 PM and 9 PM every evening. I now have evenings back and a better pipeline than I have ever had."

— Independent mortgage broker, 6 years in businessThe ROI for mortgage broker AI automation comes from four compounding sources:

- More deals from the same leads: A 34% increase in consultation bookings from existing lead volume means more revenue without increasing marketing spend. At an average commission of $3,500 per settled loan, each additional consultation booked is worth approximately $1,200 in expected revenue.

- Faster pipeline velocity: Cutting document collection time from 11 days to 3 days does not just save admin time — it gets deals settled faster, which means commission received sooner and capacity freed up for new files. Brokers report handling 2.8x as many concurrent files after automation.

- Renewal capture: A broker with 200 settled loans capturing 65% at renewal vs 22% without automation generates 43 additional renewal deals per year. At $2,800 average refinance commission, that is $120,400 in annual revenue that previously went to competitors.

- Time value: Brokers report saving 18–24 hours per week on manual admin. At a broker's billable rate equivalent of $150/hour, that is $2,700–$3,600 per week in time returned — time that can be spent on higher-value client relationships, referral partner development, and new business generation.

The total first-year ROI for a typical 1–3 broker firm implementing a full AI automation stack: $180,000–$380,000 in recovered revenue and time value, against an annual automation cost of $3,600–$8,400.

For a more granular breakdown of automation ROI in your specific context, the AI automation ROI calculator provides a structured framework applicable to mortgage brokerages of all sizes.

5 Mistakes Mortgage Brokers Make When Adopting AI

1. Automating before fixing the underlying process

Automation makes existing processes faster — including broken ones. If your lead qualification questions are vague, your AI bot will collect vague data faster. Map your ideal manual workflow before automating it. Fix the steps that do not work before putting them on autopilot.

2. Not connecting AI to a real CRM

An AI chatbot that qualifies leads but dumps them into an email inbox is not automation — it is a slightly fancier form. The value of AI comes from the data flowing directly into a structured CRM pipeline where every follow-up, stage change, and document receipt is tracked automatically. Without CRM integration, you are still doing manual data entry.

3. Over-automating the first client conversation

Mortgage clients are making the largest financial decision of their lives. The first human conversation with a broker is high-value and should not be delayed unnecessarily. Design your AI to handle qualification and scheduling — but route the client to a real broker call promptly. Do not put the advice conversation behind 8 automated messages.

4. Ignoring the renewal database

Most brokers implement lead automation first and renewal automation last (or never). This is backwards. Your renewal database is the highest-ROI, lowest-cost-per-conversion lead source you have. Set up renewal re-engagement for your existing book before spending anything on new lead generation automation.

5. Measuring the wrong metrics

The wrong metric is "number of automated messages sent." The right metrics are: consultation booking rate, document collection completion time, renewal re-engagement rate, and — the only one that ultimately matters — deals settled per broker per month. Measure those four from day one and tie your automation decisions to them.

For additional context on building end-to-end workflows that avoid these pitfalls, the guide to AI-driven support workflows covers the design principles that translate directly to mortgage broker client communication systems. The broader perspective on which business processes to automate first is also worth reviewing before you commit to a sequence.

Email and WhatsApp — The Two Channels That Drive Mortgage Pipeline

Mortgage brokers who optimise for a single communication channel leave significant pipeline velocity on the table. The two highest-performing channels in 2026 for mortgage client communication are email and WhatsApp — and they serve different purposes in the pipeline.

Email is the channel for formal communication, document delivery, and detailed rate comparison content. Clients expect to receive pre-approval letters, product comparisons, and settlement documentation by email. Automated email sequences work well for: initial application confirmation, document checklist delivery, conditional approval notification, settlement confirmation, and post-settlement check-ins. The email automations every business needs covers the core sequences that underpin a mortgage broker's communication stack.

WhatsApp is the channel for real-time engagement, reminders, and time-sensitive communication. Open rates on WhatsApp are 98% vs 22% for email. Document reminder messages, consultation booking links, rate expiry alerts, and quick-turnaround document requests all perform significantly better on WhatsApp than email. The full guide to WhatsApp Business automation covers how to use the Business API compliantly and at scale.

The most effective mortgage broker automation stacks use both channels in parallel — email for documentation and formal communication, WhatsApp for nudges, reminders, and time-sensitive action prompts. AI determines which channel to use based on the message type and the client's previous responsiveness.

The Brokers Winning in 2026 Are Not Hiring — They Are Automating

The mortgage market in 2026 is more competitive than at any point in the last decade. Rate comparison has never been easier, clients have never been more informed, and the brokers taking market share are not the ones with the biggest teams. They are the ones responding in 90 seconds at 11 PM, following up on every document automatically, and re-engaging their entire existing client base before renewal — without a single manual step.

The four workflows in this guide — lead response, pre-qualification, document collection, and renewal re-engagement — represent the core of what separates the top quartile of mortgage brokers from the rest. None of them require significant technical expertise to implement. All of them have documented ROI that exceeds automation costs within 30 days for the typical brokerage.

The only question is whether you start today or six months from now — after your competitors have used that time to capture a larger share of the same leads you are both spending money to generate.

Use the AI Business Twin for a free personalised analysis of your brokerage pipeline — including which automation workflows would have the highest impact for your specific lead volume, deal size, and client base. Takes under 10 minutes.

Frequently Asked Questions

Which tasks in a mortgage broker's workflow are easiest to automate first?

The fastest wins are lead response and pre-qualification. An AI chatbot or WhatsApp bot can respond to every inbound enquiry within 90 seconds, collect income, employment and property details, and score the lead against your lender criteria — without any broker involvement. Document collection reminders are a close second: automated SMS and email follow-ups reduce the average time to full application from 11 days to under 3.

Is AI pre-qualification accurate enough to trust for mortgage applications?

AI pre-qualification is designed as a triage tool, not a credit decision. It collects structured data (income, employment status, deposit size, existing debt), checks it against configurable lender criteria, and flags likely-eligible vs. likely-ineligible leads. The broker still makes the final recommendation. Studies show AI-assisted pre-qualification reduces time-per-application by 73% while maintaining the same approval accuracy as manual triage.

Does AI mortgage automation comply with financial services regulations?

AI automation in mortgage broking handles data collection, scheduling, reminders, and document management — activities that do not constitute regulated financial advice. The regulated advice, product recommendation, and client suitability assessment steps remain with the licensed broker. You should review the specific rules in your jurisdiction (FCA in the UK, CFPB in the US, ASIC in Australia) and ensure your AI tools are GDPR or equivalent compliant for data handling.

How do AI systems handle the document collection bottleneck?

AI document collection systems send automated reminders via SMS, email, and WhatsApp at timed intervals until each required document is received. They track exactly which documents are outstanding per client, generate personalised reminders with secure upload links, and alert the broker only when the file is complete. Brokers using this approach report the average time to complete file submission drops from 11 days to under 3 days.

Can AI help mortgage brokers win repeat business from past clients?

Yes — renewal and refinance re-engagement is one of the highest-ROI use cases for mortgage broker AI. The system monitors each client's fixed-rate expiry date and triggers a personalised outreach sequence 90, 60, and 30 days before renewal. Brokers who implement this report capturing 68% of their existing book for renewal discussions, compared to 22% without automation, because most clients do not realise their broker can help again.

What does AI mortgage automation typically cost for a small brokerage?

A full AI automation stack for a small mortgage brokerage — including CRM automation, lead response chatbot, document collection workflows, and renewal re-engagement — typically runs $300–$700 per month depending on the tools used. At a single additional deal per month, most brokerages see full ROI within the first 30 days. The Starter plan from Jogi AI at $179 per month covers the core lead response and CRM automation workflows.

How quickly can a mortgage broker get AI automation running?

A focused AI lead response and pre-qualification workflow can be live within 5 to 7 business days. Document collection automation and CRM integration typically adds another 5 to 10 days. Full pipeline automation including renewal re-engagement sequences takes 3 to 4 weeks. Most brokers see measurable results — faster lead response times and fewer lost enquiries — within the first week.